Saturday, July 14, 2012

Friday, July 13, 2012

Keynes returning?

Yves Smith has guest post by Paul Davidson author of The Keynes Solution. I generally liked the post and recommend you read it too. Here are some points I would like to make:

- Republicans abhor government but still want to get elected. Sounds like wanting the job you hate doing.

- It is never about taxes it is always about demand, if demand exists taxes are affordable. Don't eliminate taxes make them affordable by getting demand.

- Prudent regulation is good idea. Else it is like a football match without referees and ground markings.

- At 2008, either solution Keynes or otherwise would have worked. Today only alternative is Keynes.

Buy my books "Subverting Capitalism & Democracy" and "Understanding Firms".

Thursday, July 12, 2012

Combining managerial and economic theory of firm

Understanding Firm - A Manager's model of the Firm presents a new model combining managerial and economic theory of the firm.

Combining Managerial and Economic theory of the Firm

Understanding Firm - A Manager's model of the Firm presents a new model combining managerial and economic theory of the firm.

Understand Firms - A Manager's Model of the Firm

My book "Understanding Firms - A Manager's Model of the Firm has been launched.

Generations ago, the firm was conceived in the image of the army. Since then the army has moved on, but the firm hasn’t. Naturally, we experience severe difficulty while working with firms. Employees are dissatisfied, mergers fail, innovation is impossible, cost cutting is never enough and growth is not always profitable. May be we don’t understand the firm so well.

The book presents a unique model at intersection of economic and managerial theory. The model uses five elements - the concept of transaction chains, Coase transaction cost hypothesis, Porter’s bargaining power theory, a new way of profiling transaction and new types of roles undertaken by employees.

This model provides insights into which mergers will work, how to make them work, how to promote disruptive innovation, how to manage knowledge oriented teams etc. It explains why sometimes our strategy fails, why we are blind to competition and inefficiency. This model provides a new framework for thinking about firms. This framework will help us make firms better.

Tuesday, July 10, 2012

My book: Understanding Firms

My book Understanding Firms - A Manager's Model of the firm is now available.

The book presents a unique model at intersection of economic and managerial theory. The model uses five elements - the concept of transaction chains, Coase transaction cost hypothesis, Porter’s bargaining power theory, a new way of profiling transaction and new types of roles undertaken by employees.

This model provides insights into which mergers will work, how to make them work, how to promote disruptive innovation, how to manage knowledge oriented teams etc. It explains why sometimes our strategy fails, why we are blind to competition and inefficiency. This model provides a new framework for thinking about firms. This framework will help us make firms better.

I say the book is essential read for managers, investors and everyone who works in organizations. The kindle version is available at $5 (£ 3.50 and € 4.00) and print at $8 (£ 5.50 and € 6.50)

Let me know what do you think about ideas presented in the book.

Saturday, July 07, 2012

LIBOR and US Dollar

The ongoing Libor scandal is interesting to watch for other reasons as well.

First, Libor is benchmark against all the debt-risk is priced. Ok, Us treasury yields are the main benchmark, but Libor performs quite similar function. What the scandal tells us is than since last so many years this benchmark was flawed. Therefore, real Libor must be something different and hence the risk linked to it must be adequately readjusted.

Second, how will you readjust the risk without knowing what the benchmark should be. In geometry a similar problem occurs when there is a change of origin. When axes or origin are/is changed the coordinates make no sense unless you know the coordinates of new origin as per the old axis. It creates a hell lot of confusion in the geometry class when this concept is taught. Same confusion can be caused in debt markets as well. Bankers will need to reprice the debt.

Same is true with US Dollar

We really don't know what is the real value of dollar but we know value of all other currencies relative to the dollar. So watch the Libor scandal unravel will point us to important lessons for dollar. So watch carefully!

Wednesday, June 13, 2012

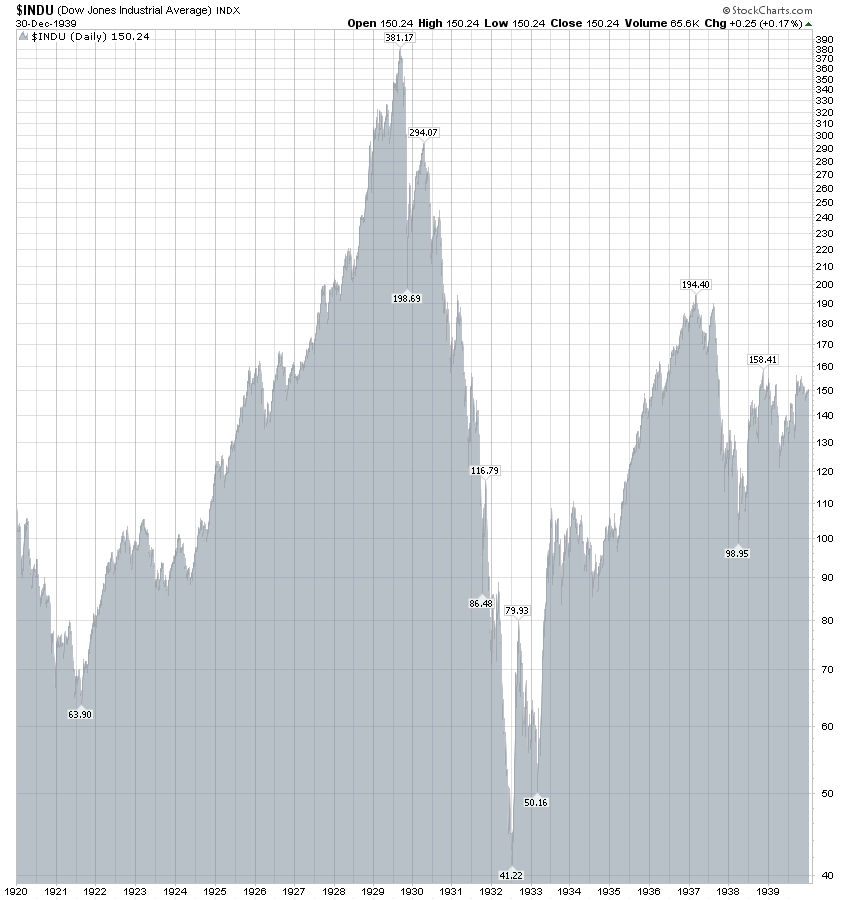

DJIA 1920-1940

A lot of people are drawing parallels between 1930-31 and today. I thought let me post a chart of DJIA over that period to understand what it means for us.

Courtesy: Stockcharts

Tuesday, June 12, 2012

Elinor Ostrom

Elinor Ostrom is no more and economics is poorer today. Her work on management of commons and economics in general was path-breaking. She was the only woman Nobel Laureate in Economics. RIP Ms. Ostrom we will never find someone as capable to carry forward your work.

Elinor Ostrom is no more and economics is poorer today. Her work on management of commons and economics in general was path-breaking. She was the only woman Nobel Laureate in Economics. RIP Ms. Ostrom we will never find someone as capable to carry forward your work.

Rahul

Monday, June 11, 2012

Parallels and differences Germany vs. EU and US vs. China

I would like to draw attention of policy watchers to this interesting parallel - What Germany is to EU, China is to US. I have raised this point earlier as well.

- Germany is the manufacturing powerhouse primed by debt-accumulation across EU just like China is manufacturing powerhouse primed by US debt.

- Both Germany and China hold government bonds in quantities that may break the bond markets and trigger concurrent run on currencies and banks.

- Both want others to follow austerity while trying to keep interest rates low and economy primed at low unemployment.

- In effect, both will have to be architects of bailouts at substantial costs to their respective tax payers. It seems unfair but it is only reasonable way out of the current problem.

Thursday, June 07, 2012

George Soros - remarks on the Euro

Rocking Jude pointed towards a recent George Soros Speech about EU crisis (among other things) via Business Insider, which I believe is a must read. Here are some diverse but important issues:

- Soros highlights "you cannot reduce the debt burden by shrinking the economy, only by growing your way out of it." which I agree with. However, those forcing the governments to austerity may do well to remember that in the end, government enjoy a kind of legitimacy that they don't. So if push comes to shove, the politicians will roast them alive and announce a victory parade while they are at it. One of the solution to a debt crisis is to eliminate the creditor. History bears witness to many such "eliminations" (a few of them quite physical).

- The objective of the economic studies should not be search for Newtonian-like laws but rather seeking engineering objectives of "fail safe" and "factor of safety" into regulation, policy and economic system as a whole. The current risk management system is falling woefully short.

- Two-level currency system: An ideal currency system, I think, may be a two level currency system. A currency at the national level should signal the relative prices of goods and services in the economy. An international currency should signal the confidence in the judgement exercised in national currency. The international currency therefore decides the relative prices of currencies and thus of everything.

- The problem of EU is that at current position it is unsustainable. It has either to go forth (towards complete integration) or go back (break-up). Mustering the political will to forth in such climate is challenging as Soros highlights.

Wednesday, June 06, 2012

Importance of Emerging markets in portfolio

Here are my comments:

- Growth is in EMs: If you use GDP growth in addition to GDP, emerging markets will come out still higher.

- Currency story: The undervalued currencies of EM economies make it good opportunity from currency gains aspect as well.

- Known trajectory: EM economies require product and services, regulations, infrastructure along well established and well understood lines. We have done such things in developed markets before and thus it is less risky.

- Less consumer leverage: One significant difference between other economies and EMs is consumer is not leveraged. In fact there is substantial class of people with good amount of savings and latent demand. Thus, once government policies are on track, you can have growth and not face deleveraging.

- Political risks: Government or political risks, to my mind are same as developed countries. All politicians are jack-asses and we have seen how politicians from any country, developed or emerging, can turn it into a banana republic. Further, some entrenched vested interest may work against developed economies in this case.

Subscribe to:

Posts (Atom)